Exhibit 99.2

www. ringenergy.com NYSE American: REI VALUE FOCUSED PROVEN STRATEGY

www.ringenergy.com NYSE American: REI Forward - Looking Statements and Cautionary Note Regarding Hydrocarbon Disclosures 2 Forward – Looking Statements This Presentation includes "forward - looking statements" within the meaning of the Private Securities Litigation Reform Act of 19 95, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. All statements, other than statements of strictly historical facts included in this Presentation constitute forwa rd - looking statements and may often, but not always, be identified by the use of such words as “may,” “will,” “should,” “could,” “intends,” “estimates,” “expects,” “anticipates,” “plans,” “project,” “guidance,” “target,” “potential,” “possible,” “p robably,” and “believes” or the negative variations thereof or comparable terminology. These forward - looking statements include statements regarding the Company's financial position, future revenues, net income, potential evaluations, bu siness strategy and plans and objectives for future operations. Forward - looking statements are subject to numerous assumptions, risks and uncertainties that may cause actual results to be materially different than any future result s e xpressed or implied in those statements. However, whether actual results and developments will conform to expectations is subject to a number of material risks and uncertainties, including but not limited to: declines in oil, natur al gas liquids or natural gas prices; the level of success in exploration, development and production activities; the timing of exploration and development expenditures; inaccuracies of reserve estimates or assumptions underlying them; revisions to rese rve estimates as a result of changes in commodity prices or production history; impacts to financial statements as a result of impairment write - downs; risks related to level of indebtedness and periodic redeterminations of the borrowing base u nder the Company’s credit facility; the impacts of hedging on results of operations; the Company’s ability to replace oil and natural gas reserves; any loss of senior management or technical personnel; and the direct and indirect impac t o n most or all of the foregoing due to the COVID - 19 pandemic. Some of the factors that could cause actual results to differ materially from expected results are described under “Risk Factors” in our 2021 annual report on Form 10 - K filed with the U.S. Securities and Exchange Commission (“SEC”) on March 16, 2022, and in our subsequent quarterly reports on Form 10 - Q and current reports on Form 8 - K. Although the Company believes that the assumptions upon which such forward - looking st atements are based are reasonable, it can give no assurance that such assumptions will prove to be correct. All forward - looking statements in this Presentation are expressly qualified by the cautionary statements and by reference to the underlying assumptions that may prove to be incorrect. The Company undertakes no obligation to publicly revise these forward - looking statements to reflect events or circumstances that arise after the date hereof, except as required by applicable law. The financial and operating estimates contained in this presentation represent our reasonable estimates as of the date of this Presentation. Neither our independen t a uditors nor any other third party has examined, reviewed or compiled the projections and, accordingly, none of the foregoing expresses an opinion or other form of assurance with respect thereto. The assumptions upon which the projection s a re based are described in more detail herein. Some of these assumptions inevitably will not materialize, and unanticipated events may occur that could affect our results. Therefore, our actual results achieved during the periods cover ed by the estimates will vary from the projected results. Prospective investors are cautioned not to place undue reliance on the estimates included herein. Cautionary Note regarding Hydrocarbon Disclosures The SEC has generally permitted oil and natural gas companies, in their filings with the SEC, to disclose proved reserves, wh ich are reserve estimates that geological and engineering data demonstrate with reasonable certainty to be recoverable in future years from known reservoirs under existing economic and operating conditions, and certain probable and possible res erv es that meet the SEC’s definitions for such terms. We use the terms “estimated ultimate recovery,” or “EURs,” “probable,” “possible,” and “non - proven” reserves, reserve “potential” or “upside” or other descriptions of volumes of reserves potentially recoverable through additional drilling or recovery techniques that the SEC’s guidelines prohibit us from including in filings with the SEC. Reference to EURs of natural gas and oil includes amounts that are not yet classified as proved reserves under SEC definitions, but that we believe should ultimately be produced and are based on previous operating experience in a given area and publicly available information relating to the operations of producers who are condu cti ng operations in these areas. These estimates are by their nature more speculative than estimates of proved reserves and accordingly are subject to substantially greater risk of being actually realized by us. Factors affecting the ul tim ate recovery of reserves that may be recovered include the scope of our drilling programs, which will be directly affected by capital availability, drilling and production costs, commodity prices, availability of services and equipment, pe rmi t expirations, transportation constraints, regulatory approvals and other factors, and actual drilling results, including geological and mechanical factors affecting recovery rates. Accordingly, actual quantities that may be recovered from our int ere sts will differ from our estimates and could be significantly less than our targeted recovery rate. In addition, our estimates may change significantly as we receive additional data. Supplemental Non - GAAP Financial Measures This Presentation includes financial measures that are not in accordance with accounting principles generally accepted in the Un ited States (“GAAP”), such as “Adjusted Net Income,” “Adjusted EBITDA,” “PV - 10,” “Free Cash Flow,” or “FCF,” and “Cash Flow from Operations.” While management believes that such measures are useful for investors, they should not be used a s a replacement for financial measures that are in accordance with GAAP. For definitions of such non - GAAP financial measures and their reconciliations to GAAP measures, please see the Appendix.

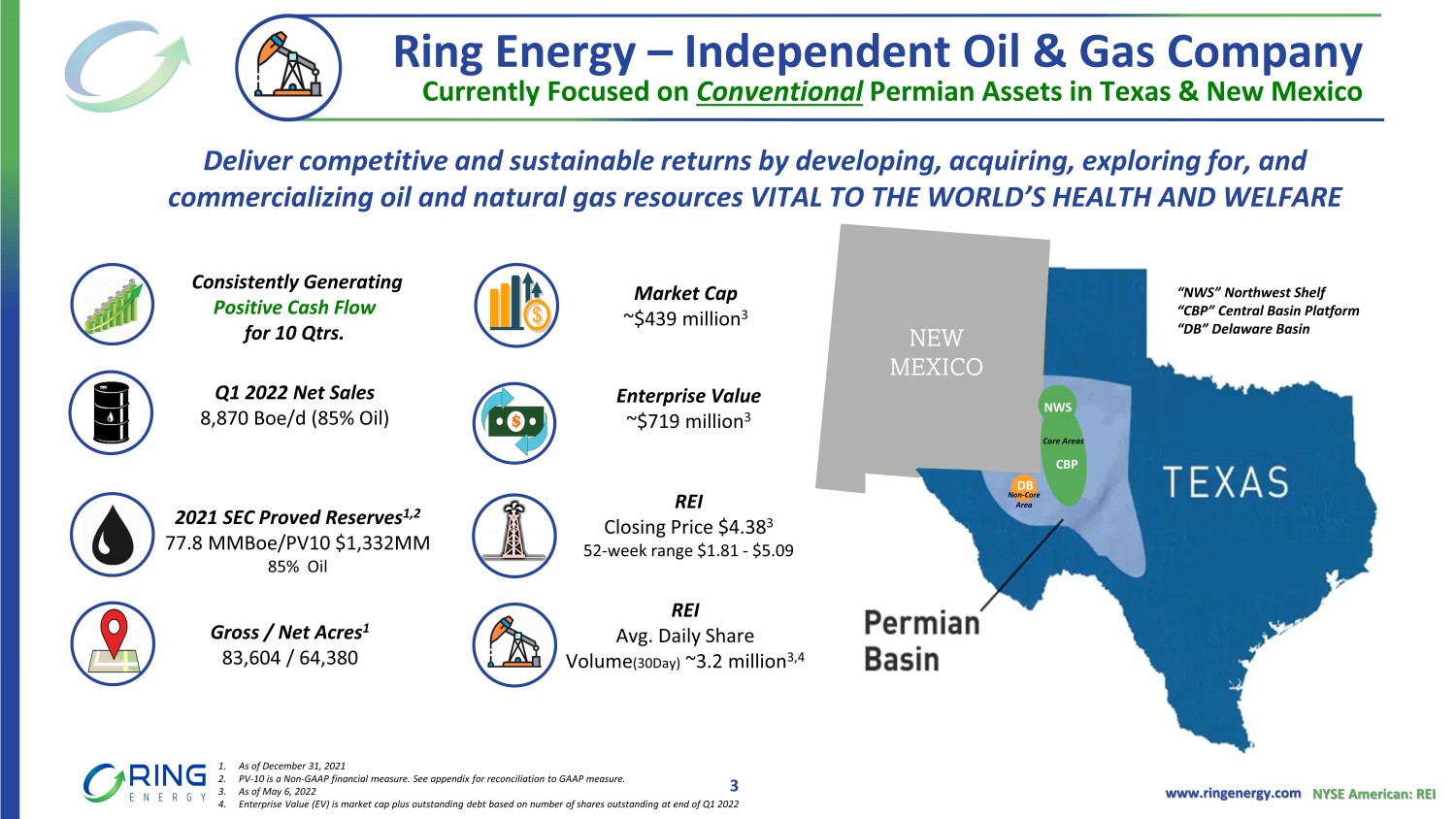

www.ringenergy.com NYSE American: REI Currently Focused on Conventional Permian Assets in Texas & New Mexico 2021 SEC Proved Reserves 1,2 77.8 MMBoe /PV10 $1,332MM 85% Oil Q1 2022 Net Sales 8,870 Boe /d (85% Oil) Gross / Net Acres 1 83,604 / 64,380 Ring Energy – Independent Oil & Gas Company Deliver competitive and sustainable returns by developing, acquiring, exploring for, and commercializing oil and natural gas resources VITAL TO THE WORLD’S HEALTH AND WELFARE 1. As of December 31, 2021 2. PV - 10 is a Non - GAAP financial measure. See appendix for reconciliation to GAAP measure. 3. As of May 6, 2022 4. Enterprise Value (EV) is market cap plus outstanding debt based on number of shares outstanding at end of Q1 2022 3 Market Cap ~$439 million 3 Consistently Generating Positive Cash Flow for 10 Qtrs. NEW MEXICO “NWS” Northwest Shelf “CBP” Central Basin Platform “DB” Delaware Basin Enterprise Value ~$719 million 3 REI Closing Price $4.38 3 52 - week range $1.81 - $5.09 REI Avg. Daily Share Volume (30Day) ~3.2 million 3,4 Non - Core Area DB CBP NWS Core Areas

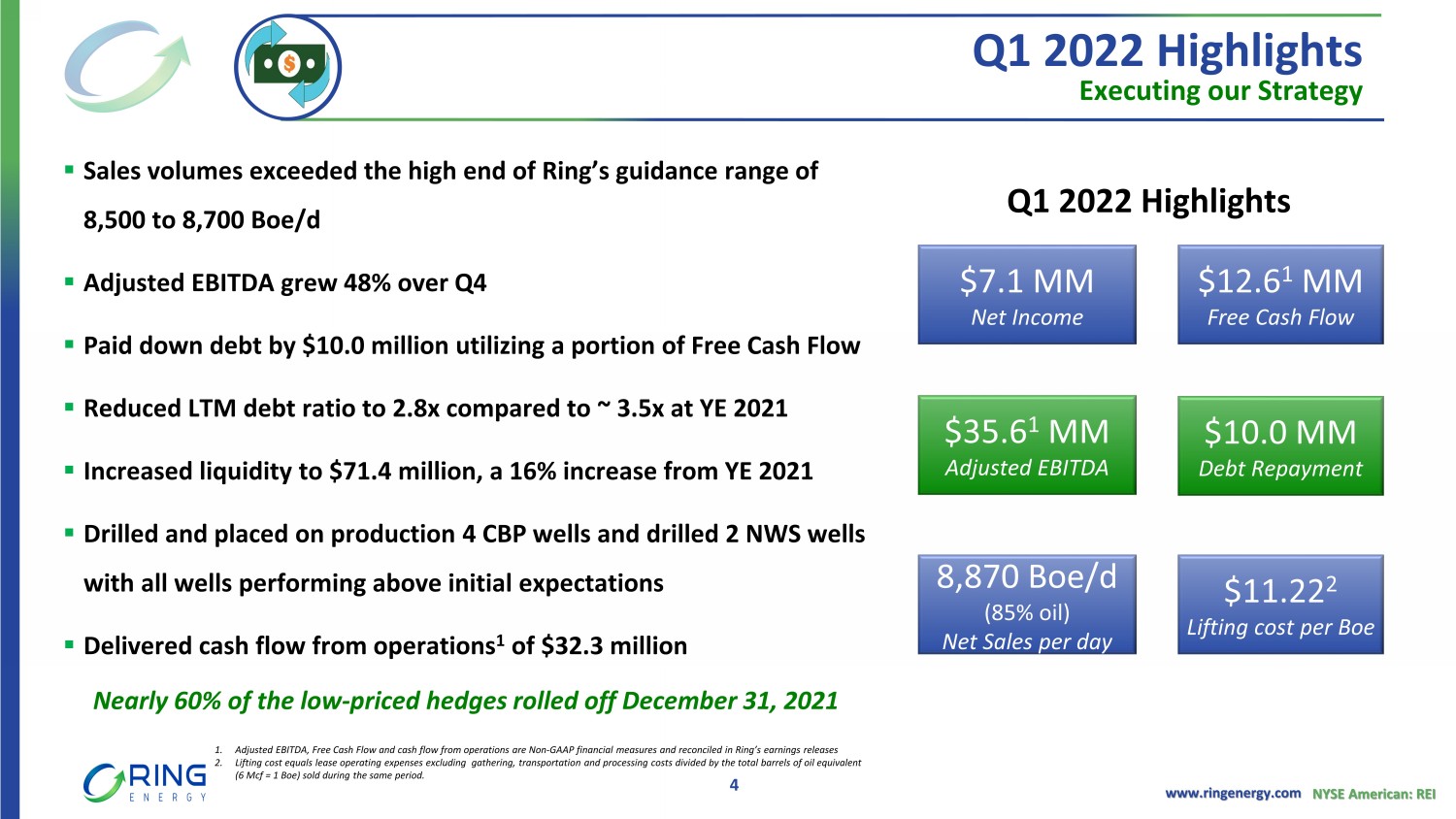

www.ringenergy.com NYSE American: REI Q1 2022 Highlights Executing our Strategy 4 ▪ Sales volumes exceeded the high end of Ring’s guidance range of 8,500 to 8,700 Boe /d ▪ Adjusted EBITDA grew 48% over Q4 ▪ Paid down debt by $10.0 million utilizing a portion of Free Cash Flow ▪ Reduced LTM debt ratio to 2.8x compared to ~ 3.5x at YE 2021 ▪ Increased liquidity to $71.4 million, a 16% increase from YE 2021 ▪ Drilled and placed on production 4 CBP wells and drilled 2 NWS wells with all wells performing above initial expectations ▪ Delivered cash flow from operations 1 of $32.3 million $12.6 1 MM Free Cash Flow $35.6 1 MM Adjusted EBITDA $7.1 MM Net Income $10.0 MM Debt Repayment 8 ,870 Boe /d (85% oil) Net Sales per day $11.22 2 Lifting cost per Boe 1. Adjusted EBITDA, Free Cash Flow and cash flow from operations are Non - GAAP financial measures and reconciled in Ring’s earnings releases 2. Lifting cost equals lease operating expenses excluding gathering, transportation and processing costs divided by the total b arr els of oil equivalent (6 Mcf = 1 Boe ) sold during the same period. Q1 2022 Highlights Nearly 60% of the low - priced hedges rolled off December 31, 2021

www.ringenergy.com NYSE American: REI Committed to ESG Issued Inaugural ESG Report in Q4 2021 5

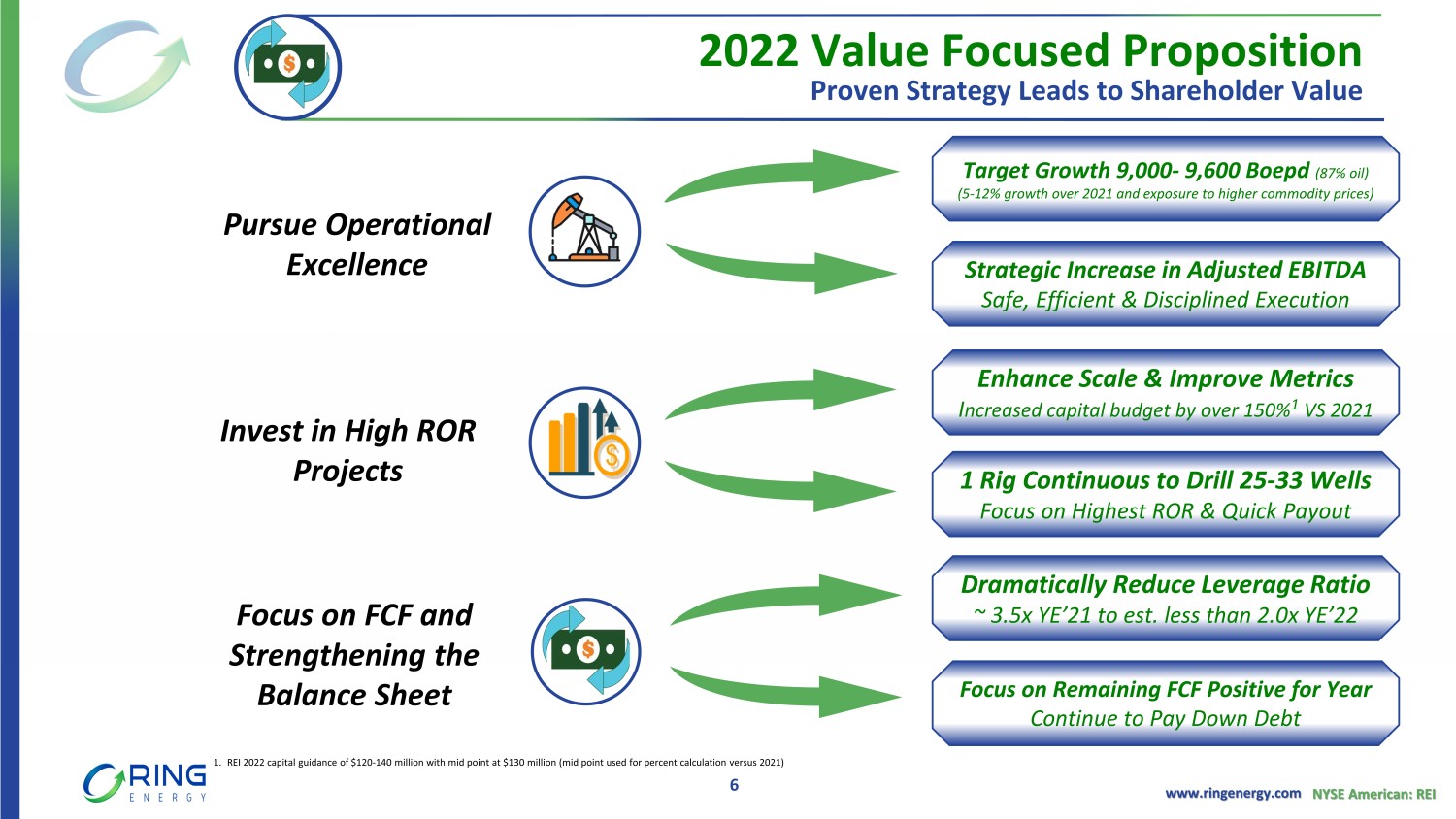

www.ringenergy.com NYSE American: REI Focus on FCF and Strengthening the Balance Sheet Invest in High ROR Projects 1 Rig Continuous to Drill 25 - 33 Wells Focus on Highest ROR & Quick Payout Strategic Increase in Adjusted EBITDA Safe, Efficient & Disciplined Execution Target Growth 9,000 - 9,600 Boepd (87% oil) (5 - 12% growth over 2021 and exposure to higher commodity prices) Dramatically Reduce Leverage Ratio ~ 3.5x YE’21 to est. less than 2.0x YE’22 Focus on Remaining FCF Positive for Year Continue to Pay Down Debt 6 Enhance Scale & Improve Metrics I ncreased capital budget by over 150% 1 VS 2021 Proven Strategy Leads to Shareholder Value 2022 Value Focused Proposition 1. REI 2022 capital guidance of $120 - 140 million with mid point at $130 million (mid point used for percent calculation versus 2021 ) Pursue Operational Excellence

Asset Areas

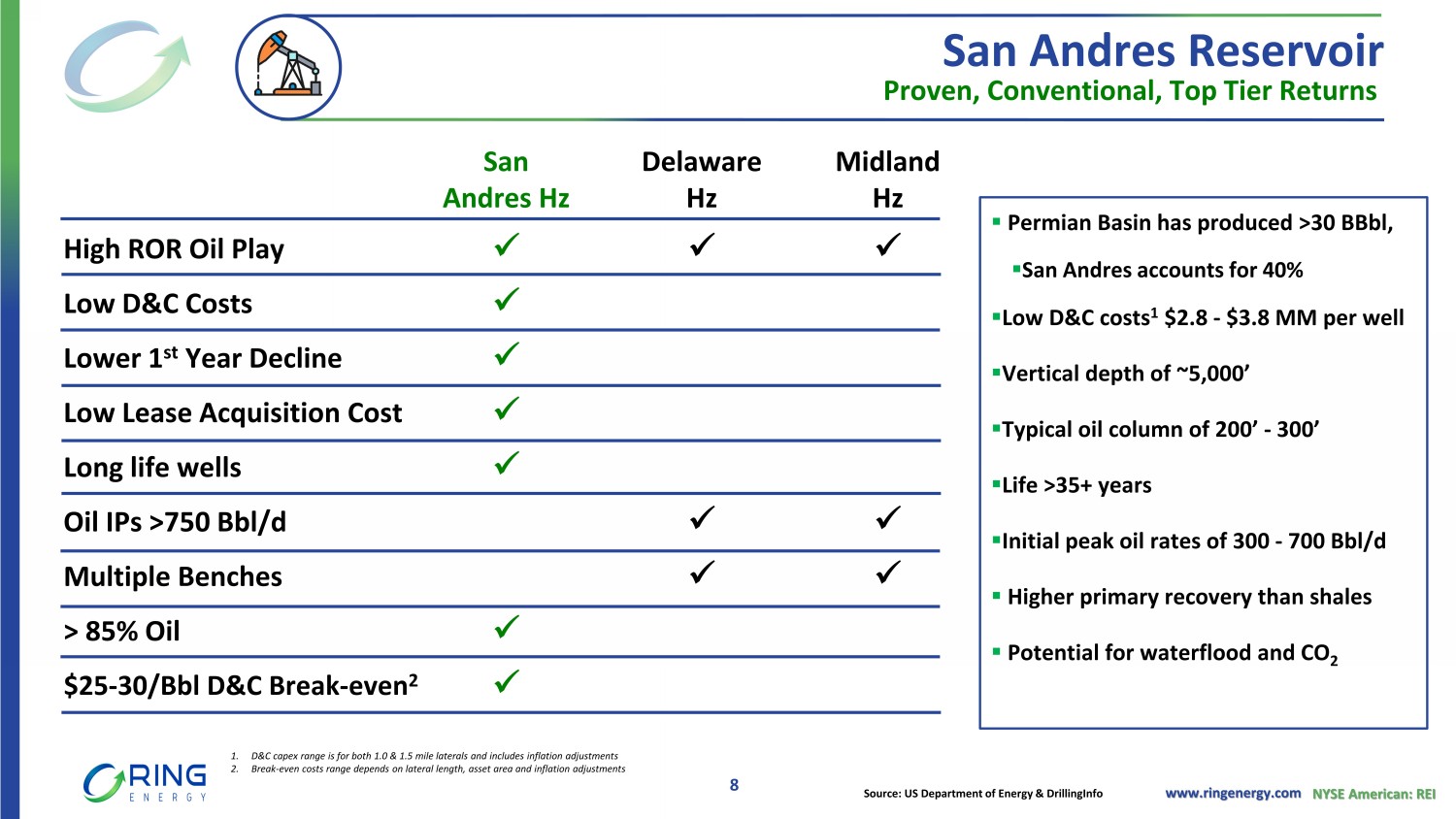

www.ringenergy.com NYSE American: REI Proven, Conventional, Top Tier Returns San Andres Hz Delaware Hz Midland Hz High ROR Oil Play x x x Low D&C Costs x Lower 1 st Year Decline x Low Lease Acquisition Cost x Long life wells x Oil IPs >750 Bbl /d x x Multiple Benches x x > 85% Oil x $25 - 30/ Bbl D&C Break - even 2 x ▪ Permian Basin has produced >30 BBbl , ▪ San Andres accounts for 40% ▪ Low D&C costs 1 $2.8 - $3.8 MM per well ▪ Vertical depth of ~5,000’ ▪ Typical oil column of 200’ - 300’ ▪ Life >35+ years ▪ Initial peak oil rates of 300 - 700 Bbl/d ▪ Higher primary recovery than shales ▪ Potential for waterflood and CO 2 Source: US Department of Energy & DrillingInfo 8 San Andres Reservoir 1. D&C capex range is for both 1.0 & 1.5 mile laterals and includes inflation adjustments 2. Break - even costs range depends on lateral length, asset area and inflation adjustments

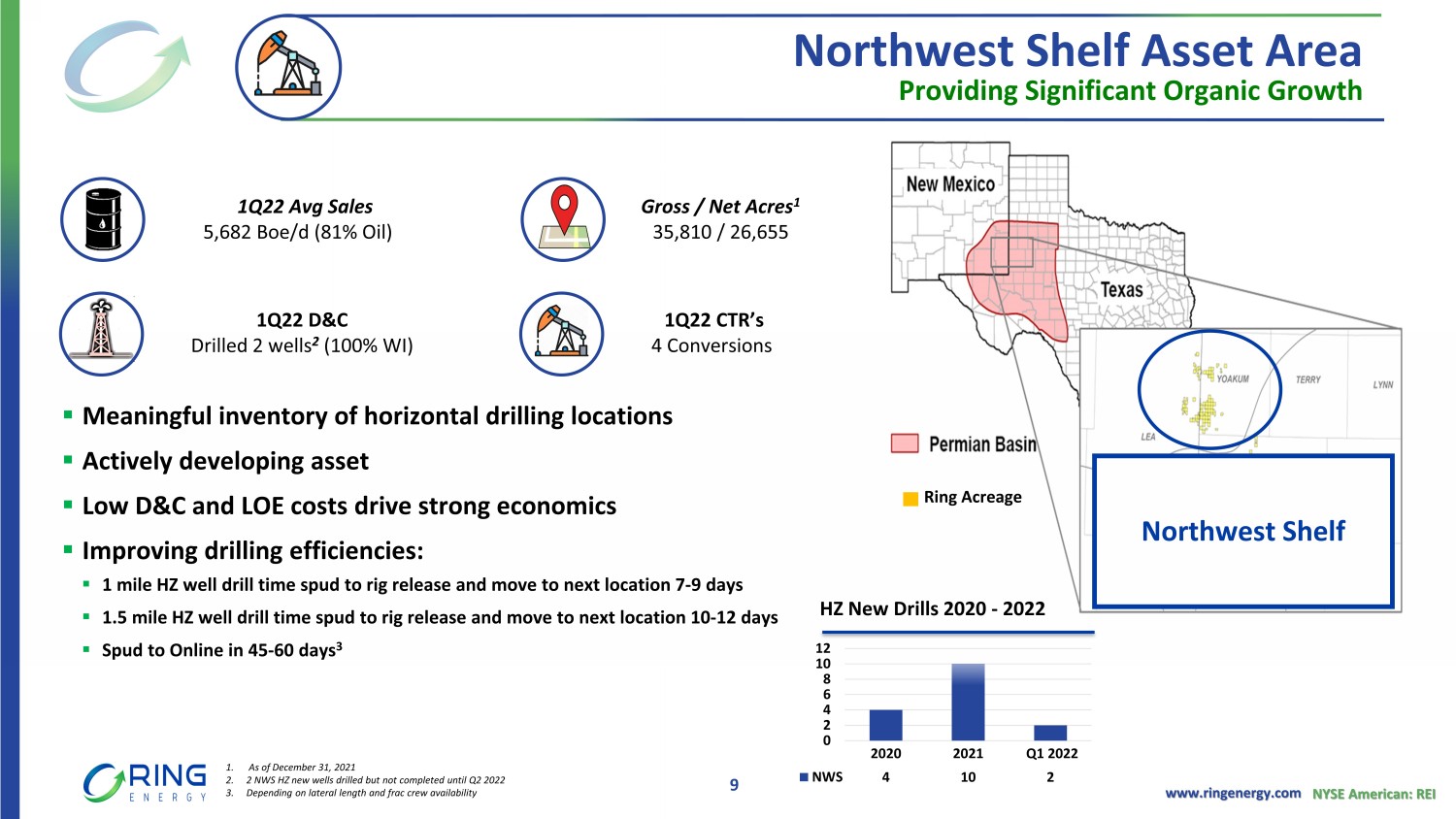

www.ringenergy.com NYSE American: REI ▪ Meaningful inventory of horizontal drilling locations ▪ Actively developing asset ▪ Low D&C and LOE costs drive strong economics ▪ Improving drilling efficiencies: ▪ 1 mile HZ well drill time spud to rig release and move to next location 7 - 9 days ▪ 1.5 mile HZ well drill time spud to rig release and move to next location 10 - 12 days ▪ Spud to Online in 45 - 60 days 3 Providing Significant Organic Growth 1Q22 Avg Sales 5,682 Boe /d (81% Oil) 1Q22 D&C Drilled 2 wells 2 (100% WI) Gross / Net Acres 1 35,810 / 26,655 Northwest Shelf Asset Area 9 1Q22 CTR’s 4 Conversions 1. As of December 31, 2021 2. 2 NWS HZ new wells drilled but not completed until Q2 2022 3. Depending on lateral length and frac crew availability Ring Acreage Northwest Shelf 2020 2021 Q1 2022 NWS 4 10 2 0 2 4 6 8 10 12 HZ New Drills 2020 - 2022

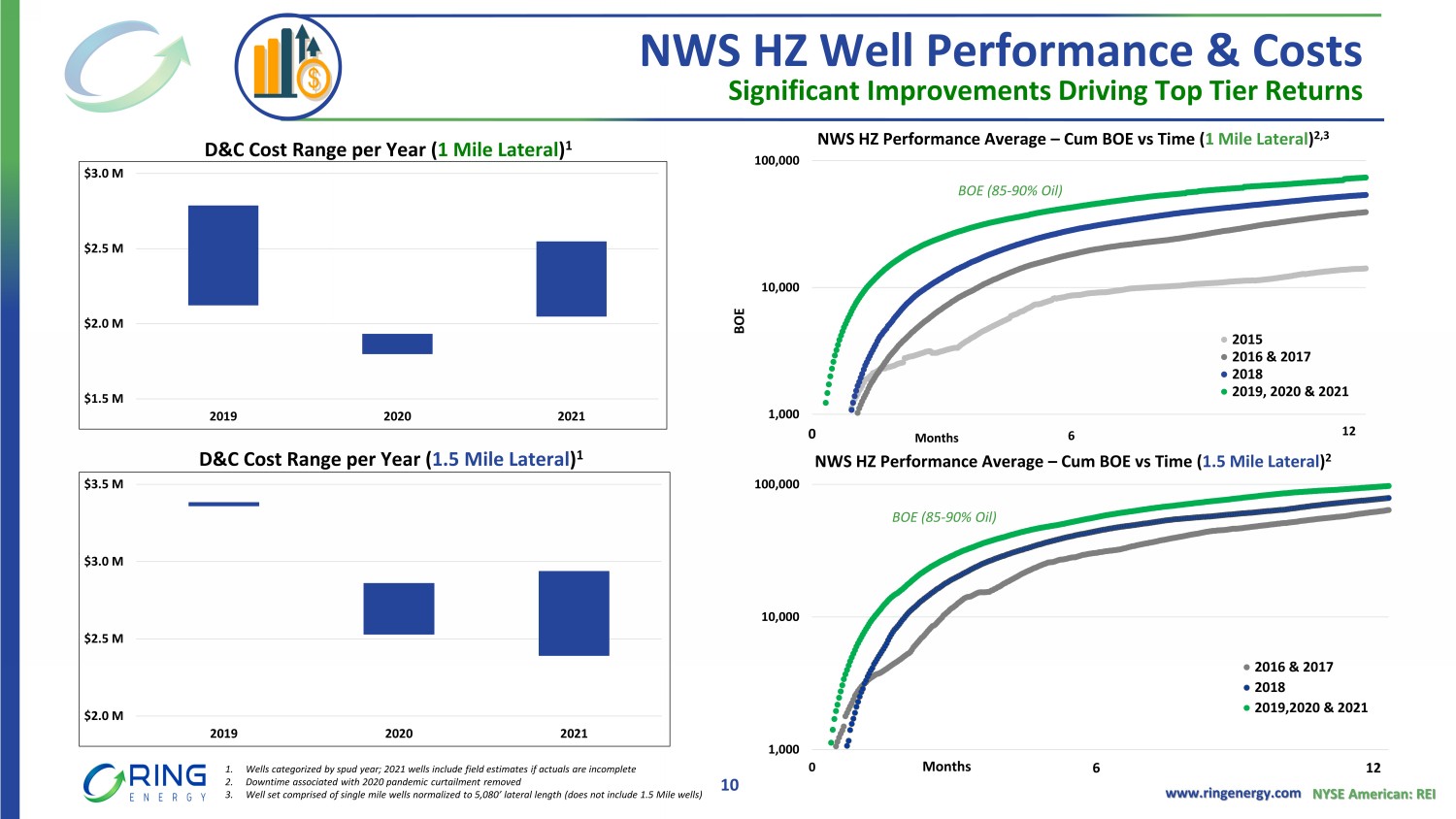

www.ringenergy.com NYSE American: REI 1,000 10,000 100,000 0 180 360 2016 & 2017 2018 2019,2020 & 2021 Months 6 12 BOE (85 - 90% Oil) 1,000 10,000 100,000 0 180 360 2015 2016 & 2017 2018 2019, 2020 & 2021 $2.0 M $2.5 M $3.0 M $3.5 M 2019 2020 2021 NWS HZ Well Performance & Costs Significant Improvements Driving Top Tier Returns 10 D&C Cost Range per Year ( 1 Mile Lateral ) 1 NWS HZ Performance Average – Cum BOE vs Time ( 1 Mile Lateral ) 2,3 1. Wells categorized by spud year; 2021 wells include field estimates if actuals are incomplete 2. Downtime associated with 2020 pandemic curtailment removed 3. Well set comprised of single mile wells normalized to 5,080’ lateral length (does not include 1.5 Mile wells) ~530 Avg ~410 Avg ~420 Avg $1.5 M $2.0 M $2.5 M $3.0 M 2019 2020 2021 D&C Cost Range per Year ( 1.5 Mile Lateral ) 1 BOE (85 - 90% Oil) Months 6 12 BOE NWS HZ Performance Average – Cum BOE vs Time ( 1.5 Mile Lateral ) 2

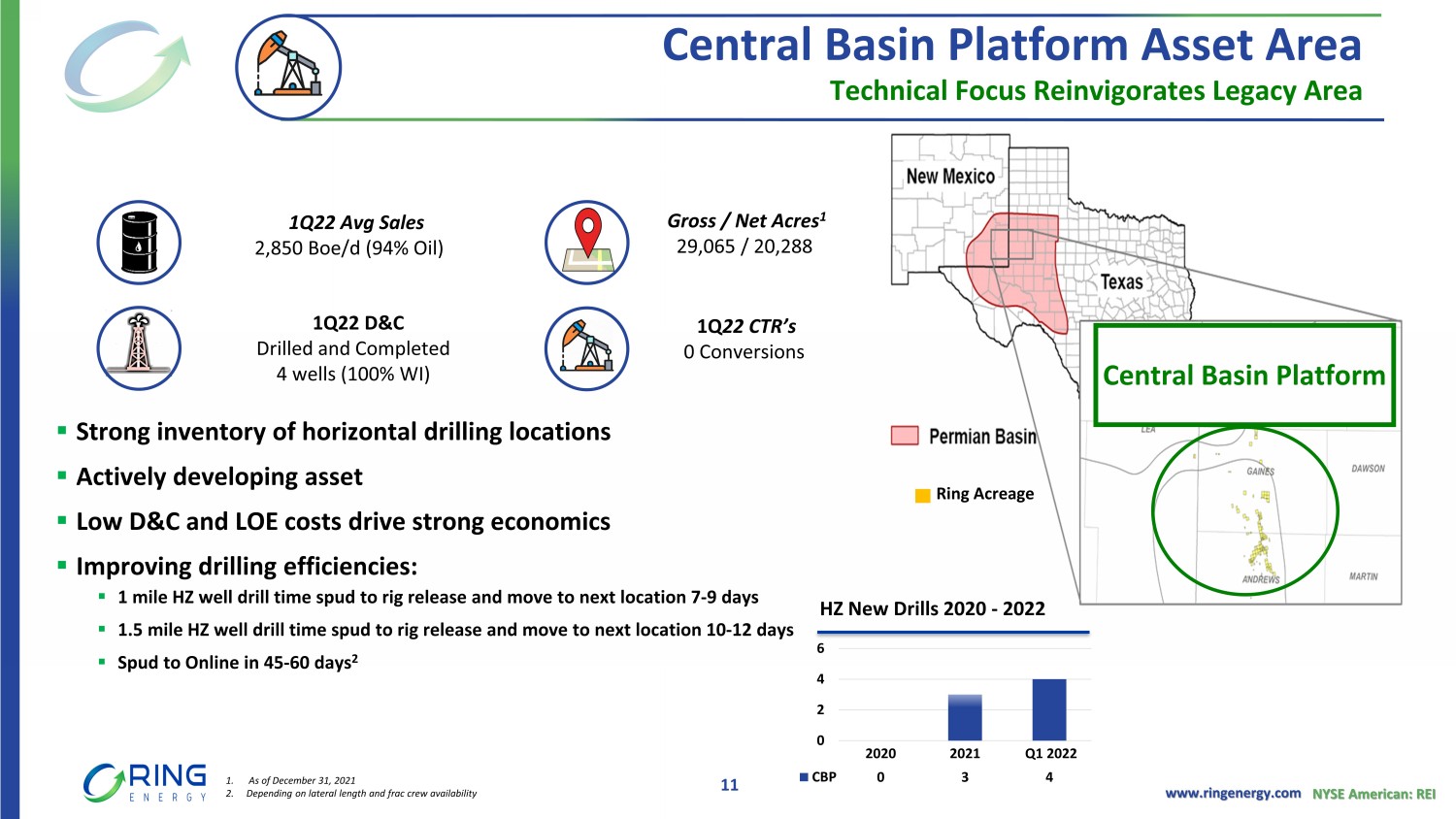

www.ringenergy.com NYSE American: REI 1Q22 Avg Sales 2,850 Boe /d (94% Oil) 1Q 22 CTR’s 0 Conversions 1Q22 D&C Drilled and Completed 4 wells (100% WI) Gross / Net Acres 1 29,065 / 20,288 Technical Focus Reinvigorates Legacy Area Central Basin Platform Asset Area 11 Ring Acreage Central Basin Platform 1. As of December 31, 2021 2. Depending on lateral length and frac crew availability ▪ Strong inventory of horizontal drilling locations ▪ Actively developing asset ▪ Low D&C and LOE costs drive strong economics ▪ Improving drilling efficiencies: ▪ 1 mile HZ well drill time spud to rig release and move to next location 7 - 9 days ▪ 1.5 mile HZ well drill time spud to rig release and move to next location 10 - 12 days ▪ Spud to Online in 45 - 60 days 2 2020 2021 Q1 2022 CBP 0 3 4 0 2 4 6 HZ New Drills 2020 - 2022

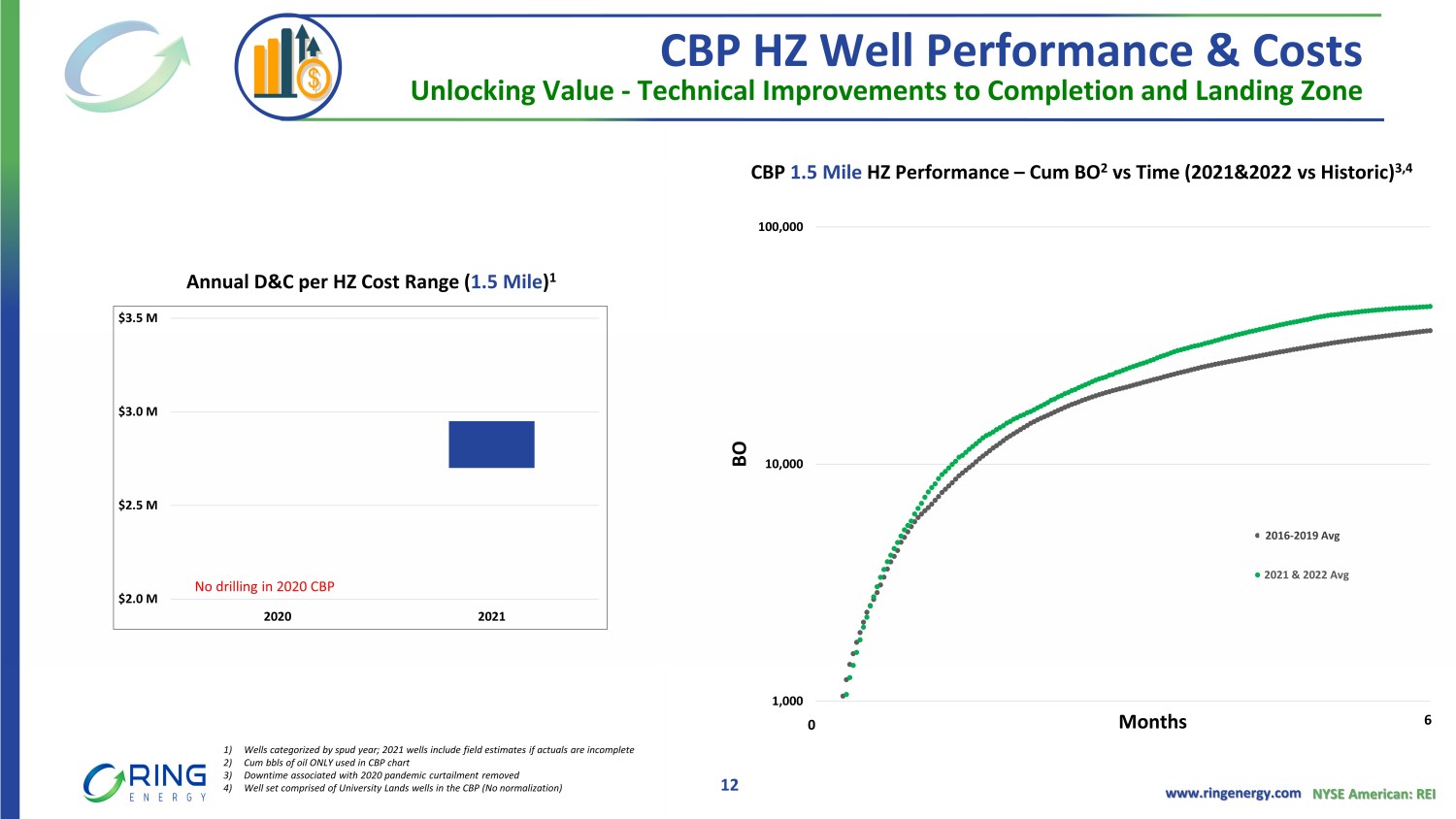

www.ringenergy.com NYSE American: REI CBP HZ Well Performance & Costs Unlocking Value - Technical Improvements to Completion and Landing Zone 12 Annual D&C per HZ Cost Range ( 1.5 Mile ) 1 ~530 Avg ~410 Avg ~420 Avg 2021 New Drills 1 Mile Wells 1.5 Mile Wells 2021 CBP New Drill (1.5 mile) HZ wells are outperforming compared to most of the historic CBP HZ wells 1) Wells categorized by spud year; 2021 wells include field estimates if actuals are incomplete 2) Cum bbls of oil ONLY used in CBP chart 3) Downtime associated with 2020 pandemic curtailment removed 4) Well set comprised of University Lands wells in the CBP (No normalization) $2.0 M $2.5 M $3.0 M $3.5 M 2020 2021 No drilling in 2020 CBP BO Need to Update 1,000 10,000 100,000 0 180 2016 - 2020 Avg 2021 & 2022 Avg CBP 1.5 Mile HZ Performance – Cum BO 2 vs Time (2021&2022 vs Historic) 3,4 6 Months 0 2016 - 2019 Avg

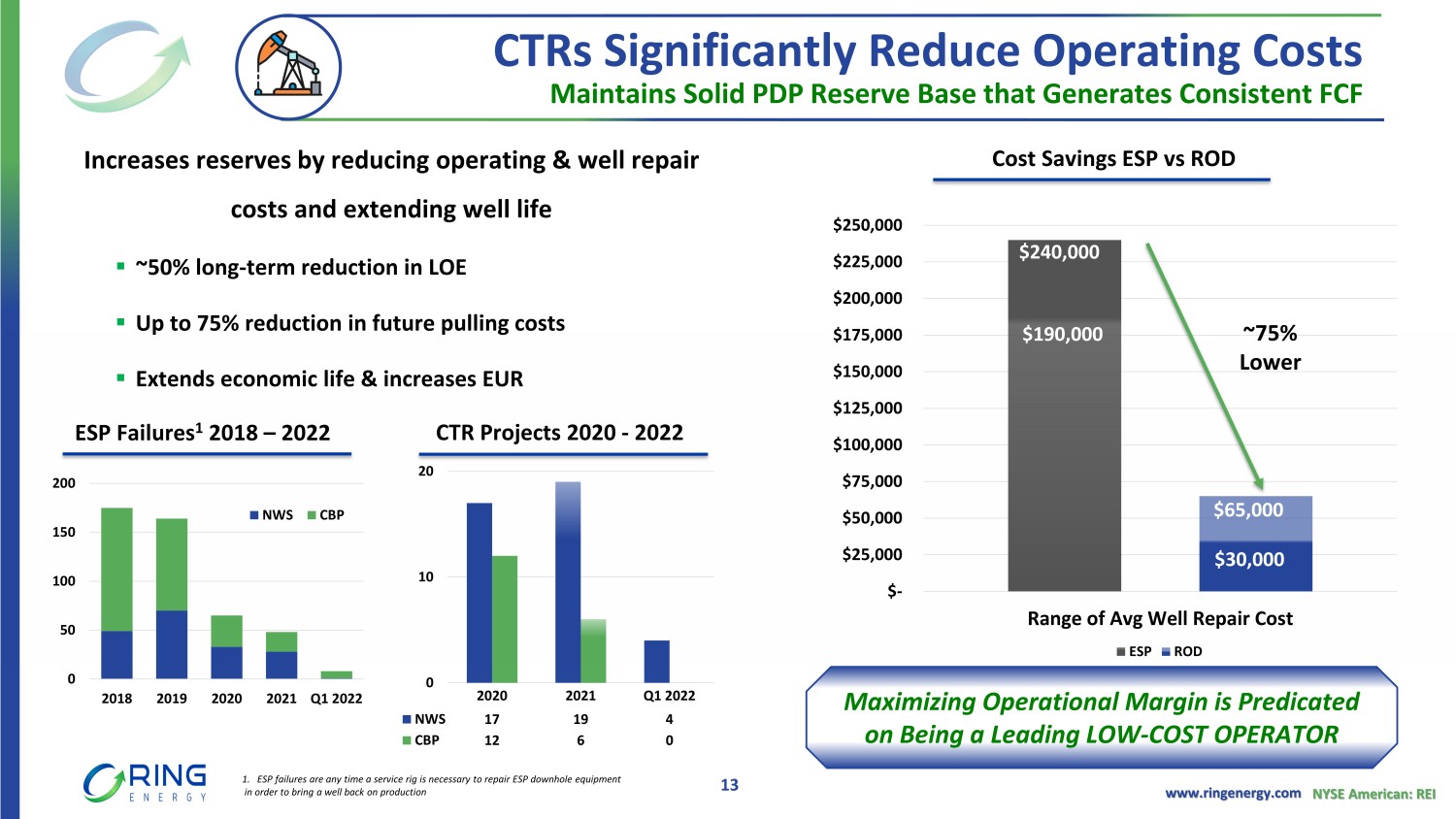

www.ringenergy.com NYSE American: REI 0 50 100 150 200 2018 2019 2020 2021 Q1 2022 NWS CBP Maintains Solid PDP Reserve Base that Generates Consistent FCF Increases reserves by reducing operating & well repair costs and extending well life ▪ ~50% long - term reduction in LOE ▪ Up to 75% reduction in future pulling costs ▪ Extends economic life & increases EUR CTRs Significantly Reduce Operating Costs 2020 2021 Q1 2022 NWS 17 19 4 CBP 12 6 0 0 10 20 13 $- $25,000 $50,000 $75,000 $100,000 $125,000 $150,000 $175,000 $200,000 $225,000 $250,000 Range of Avg Well Repair Cost ESP ROD $190,000 $65,000 $30,000 Cost Savings ESP vs ROD Maximizing Operational Margin is Predicated on Being a Leading LOW - COST OPERATOR ~75% Lower $240,000 CTR Projects 2020 - 2022 ESP Failures 1 2018 – 2022 1. ESP failures are any time a service rig is necessary to repair ESP downhole equipment in order to bring a well back on production

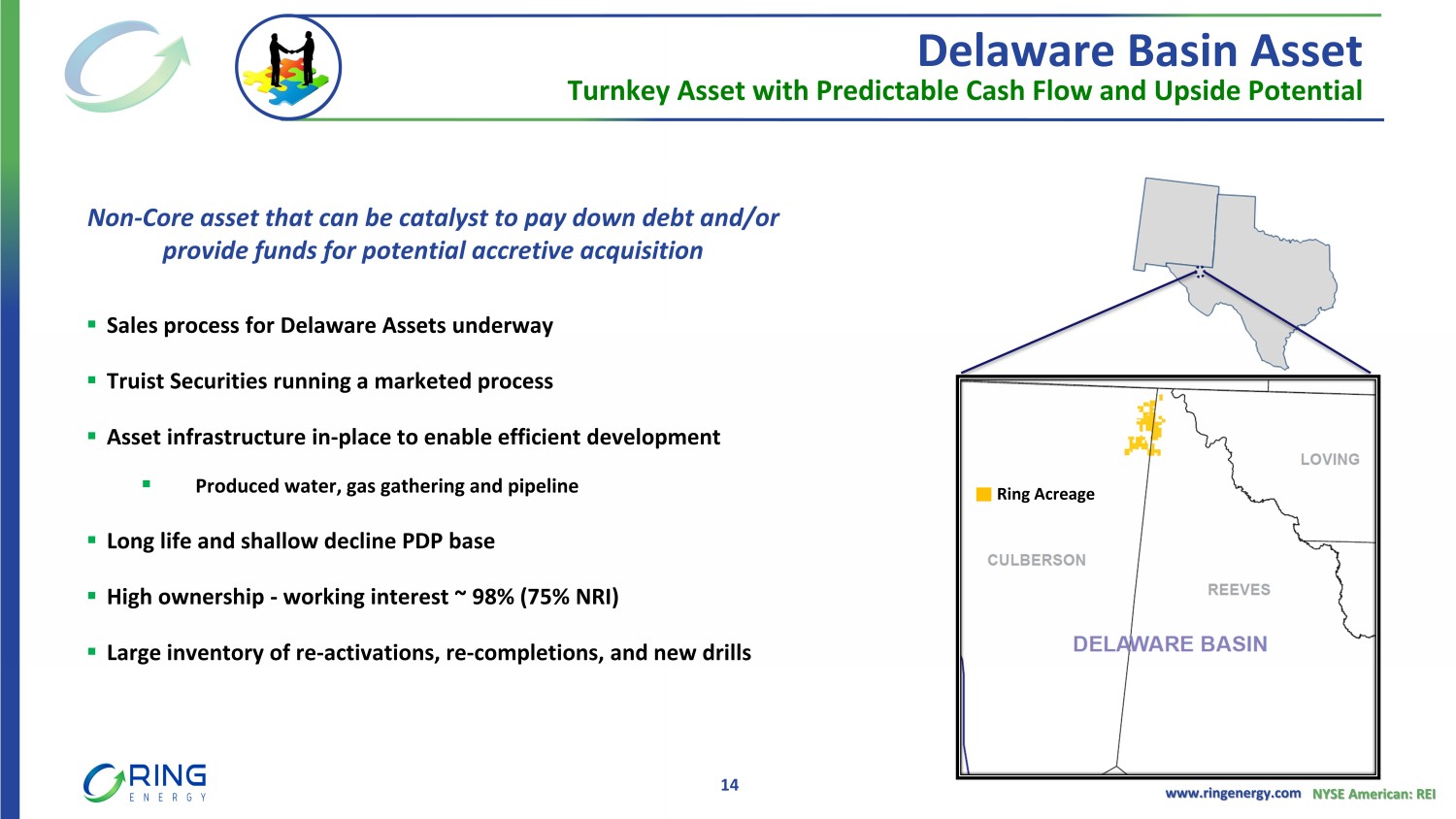

www.ringenergy.com NYSE American: REI Turnkey Asset with Predictable Cash Flow and Upside Potential Delaware Basin Asset 14 ▪ Sales process for Delaware Assets underway ▪ Truist Securities running a marketed process ▪ Asset infrastructure in - place to enable efficient development ▪ Produced water, gas gathering and pipeline ▪ Long life and shallow decline PDP base ▪ High ownership - working interest ~ 98% (75% NRI) ▪ Large inventory of re - activations, re - completions, and new drills Ring Acreage Non - Core asset that can be catalyst to pay down debt and/or provide funds for potential accretive acquisition

Financials

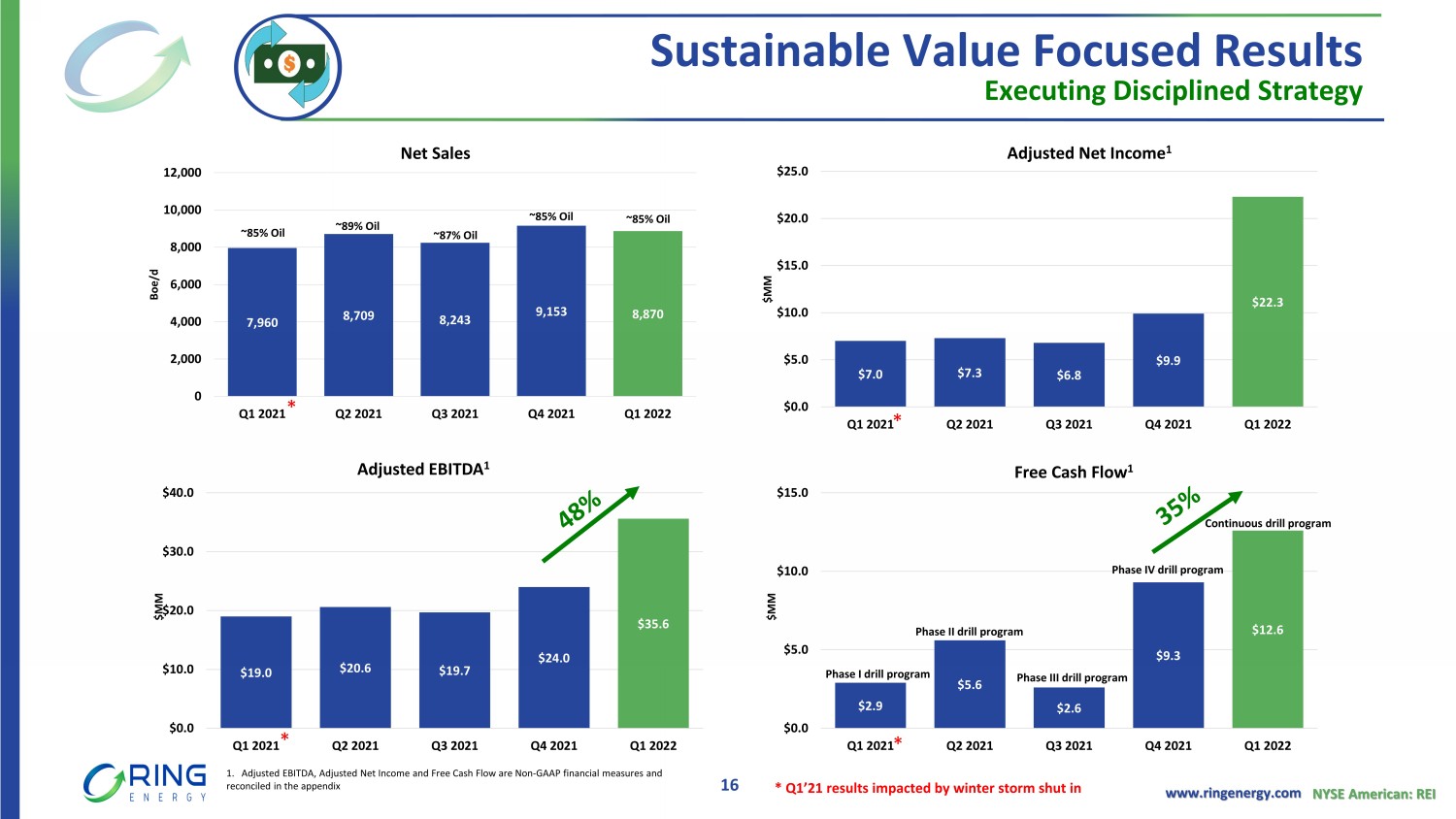

www.ringenergy.com NYSE American: REI Sustainable Value Focused Results 7,960 8,709 8,243 9,153 8,870 0 2,000 4,000 6,000 8,000 10,000 12,000 Q1 2021 Q2 2021 Q3 2021 Q4 2021 Q1 2022 Boe /d Net Sales $7.0 $7.3 $6.8 $9.9 $22.3 $0.0 $5.0 $10.0 $15.0 $20.0 $25.0 Q1 2021 Q2 2021 Q3 2021 Q4 2021 Q1 2022 $MM Adjusted Net Income 1 $19.0 $20.6 $19.7 $24.0 $35.6 $0.0 $10.0 $20.0 $30.0 $40.0 Q1 2021 Q2 2021 Q3 2021 Q4 2021 Q1 2022 $MM Adjusted EBITDA 1 $2.9 $5.6 $2.6 $9.3 $12.6 $0.0 $5.0 $10.0 $15.0 Q1 2021 Q2 2021 Q3 2021 Q4 2021 Q1 2022 $MM Free Cash Flow 1 Executing Disciplined Strategy 16 1. Adjusted EBITDA, Adjusted Net Income and Free Cash Flow are Non - GAAP financial measures and reconciled in the appendix * Q1’21 results impacted by winter storm shut in Phase I drill program * * * * Phase II drill program ~85% Oil ~87% Oil ~89% Oil ~85% Oil Phase III drill program ~85% Oil Phase IV drill program Continuous drill program

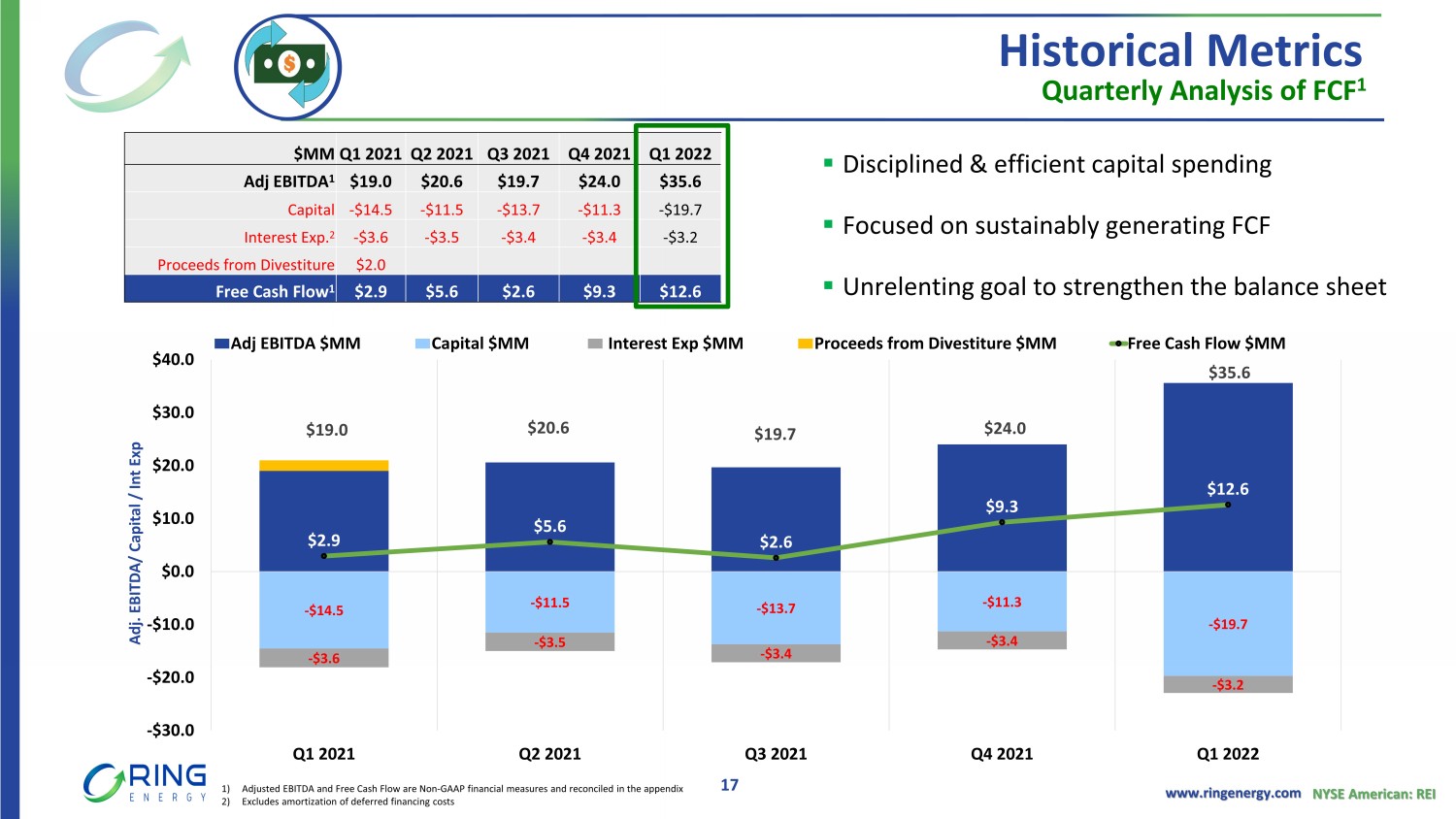

www.ringenergy.com NYSE American: REI Historical Metrics Quarterly Analysis of FCF 1 $MM Q1 2021 Q2 2021 Q3 2021 Q4 2021 Q1 2022 Adj EBITDA 1 $19.0 $20.6 $19.7 $24.0 $35.6 Capital - $14.5 - $11.5 - $13.7 - $11.3 - $19.7 Interest Exp. 2 - $3.6 - $3.5 - $3.4 - $3.4 - $3.2 Proceeds from Divestiture $2.0 Free Cash Flow 1 $2.9 $5.6 $2.6 $9.3 $12.6 17 $19.0 $20.6 $19.7 $24.0 $35.6 - $14.5 - $11.5 - $13.7 - $11.3 - $19.7 - $3.6 - $3.5 - $3.4 - $3.4 - $3.2 $2.9 $5.6 $2.6 $9.3 $12.6 -$30.0 -$20.0 -$10.0 $0.0 $10.0 $20.0 $30.0 $40.0 Q1 2021 Q2 2021 Q3 2021 Q4 2021 Q1 2022 Adj. EBITDA/ Capital / Int Exp Adj EBITDA $MM Capital $MM Interest Exp $MM Proceeds from Divestiture $MM Free Cash Flow $MM ▪ Disciplined & efficient capital spending ▪ Focused on sustainably generating FCF ▪ Unrelenting goal to strengthen the balance sheet 1) Adjusted EBITDA and Free Cash Flow are Non - GAAP financial measures and reconciled in the appendix 2) Excludes amortization of deferred financing costs

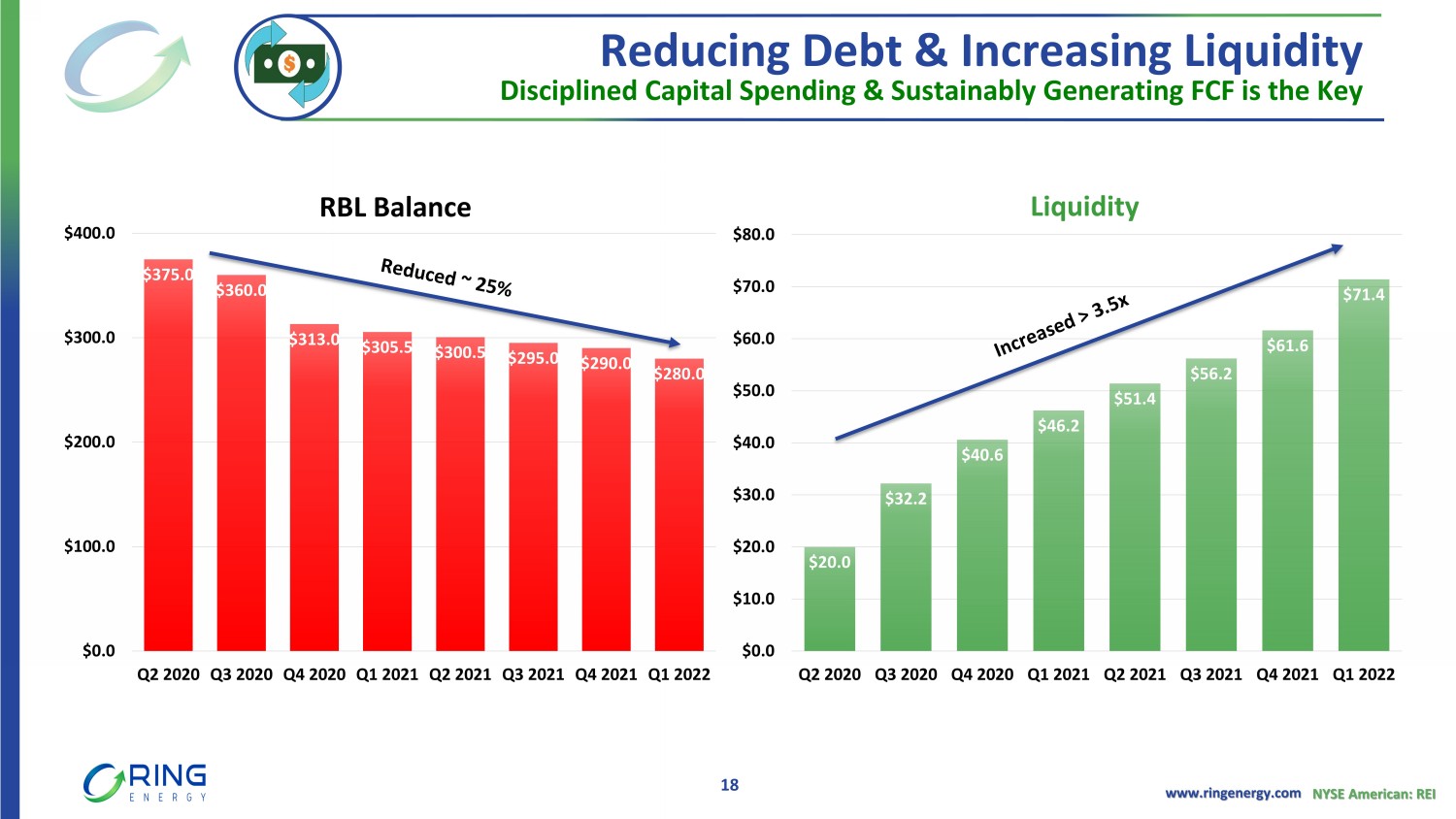

www.ringenergy.com NYSE American: REI $375.0 $360.0 $313.0 $305.5 $300.5 $295.0 $290.0 $280.0 $0.0 $100.0 $200.0 $300.0 $400.0 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021 Q3 2021 Q4 2021 Q1 2022 RBL Balance $313 MM outstanding debt with $36 MM in Surplus Cash Reducing Debt & Increasing Liquidity Disciplined Capital Spending & Sustainably Generating FCF is the Key 18 $20.0 $32.2 $40.6 $46.2 $51.4 $56.2 $61.6 $71.4 $0.0 $10.0 $20.0 $30.0 $40.0 $50.0 $60.0 $70.0 $80.0 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021 Q3 2021 Q4 2021 Q1 2022 Liquidity

www.ringenergy.com NYSE American: REI Value Proposition 2022 and Beyond Positioned for Substantial Increase in Revenue and FCF Pivoting to Continuous, High - Return Organic Growth Pursuing Acquisition Opportunities to Increase Scale and Lower Break - Even Costs 19

Appendix

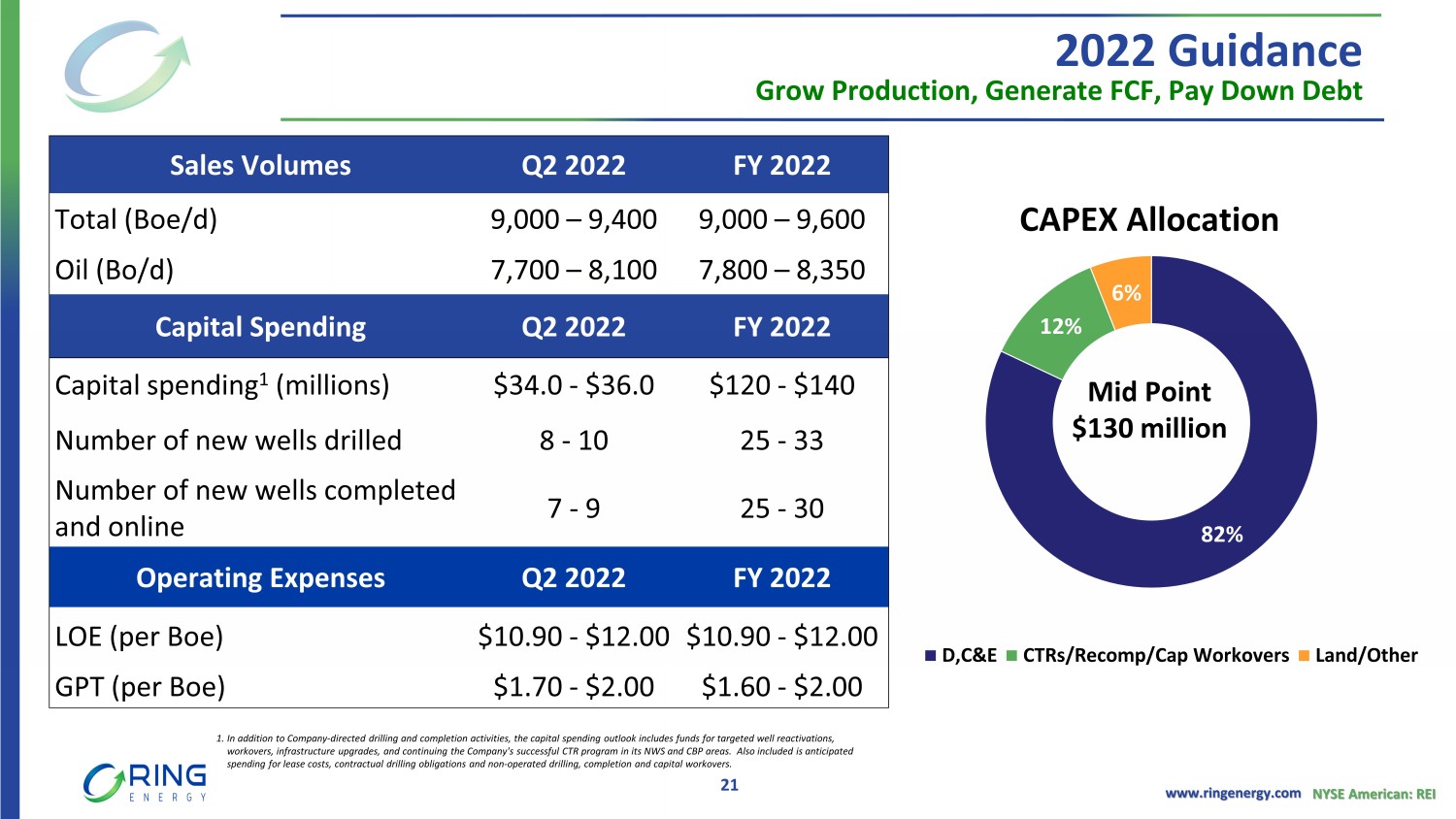

www.ringenergy.com NYSE American: REI 82% 12% 6% D,C&E CTRs/Recomp/Cap Workovers Land/Other CAPEX Allocation Mid Point $130 million 2022 Guidance Grow Production, Generate FCF, Pay Down Debt 21 Sales Volumes Q2 2022 FY 2022 Total ( Boe /d) 9,000 – 9,400 9,000 – 9,600 Oil (Bo/d) 7,700 – 8,100 7,800 – 8,350 Capital Spending Q2 2022 FY 2022 Capital spending 1 (millions) $34.0 - $36.0 $120 - $140 Number of new wells drilled 8 - 10 25 - 33 Number of new wells completed and online 7 - 9 25 - 30 Operating Expenses Q2 2022 FY 2022 LOE (per Boe ) $10.90 - $12.00 $10.90 - $12.00 GPT (per Boe ) $1.70 - $2.00 $1.60 - $2.00 1. In addition to Company - directed drilling and completion activities, the capital spending outlook includes funds for targeted wel l reactivations, workovers, infrastructure upgrades, and continuing the Company's successful CTR program in its NWS and CBP areas. Also inclu ded is anticipated spending for lease costs, contractual drilling obligations and non - operated drilling, completion and capital workovers.

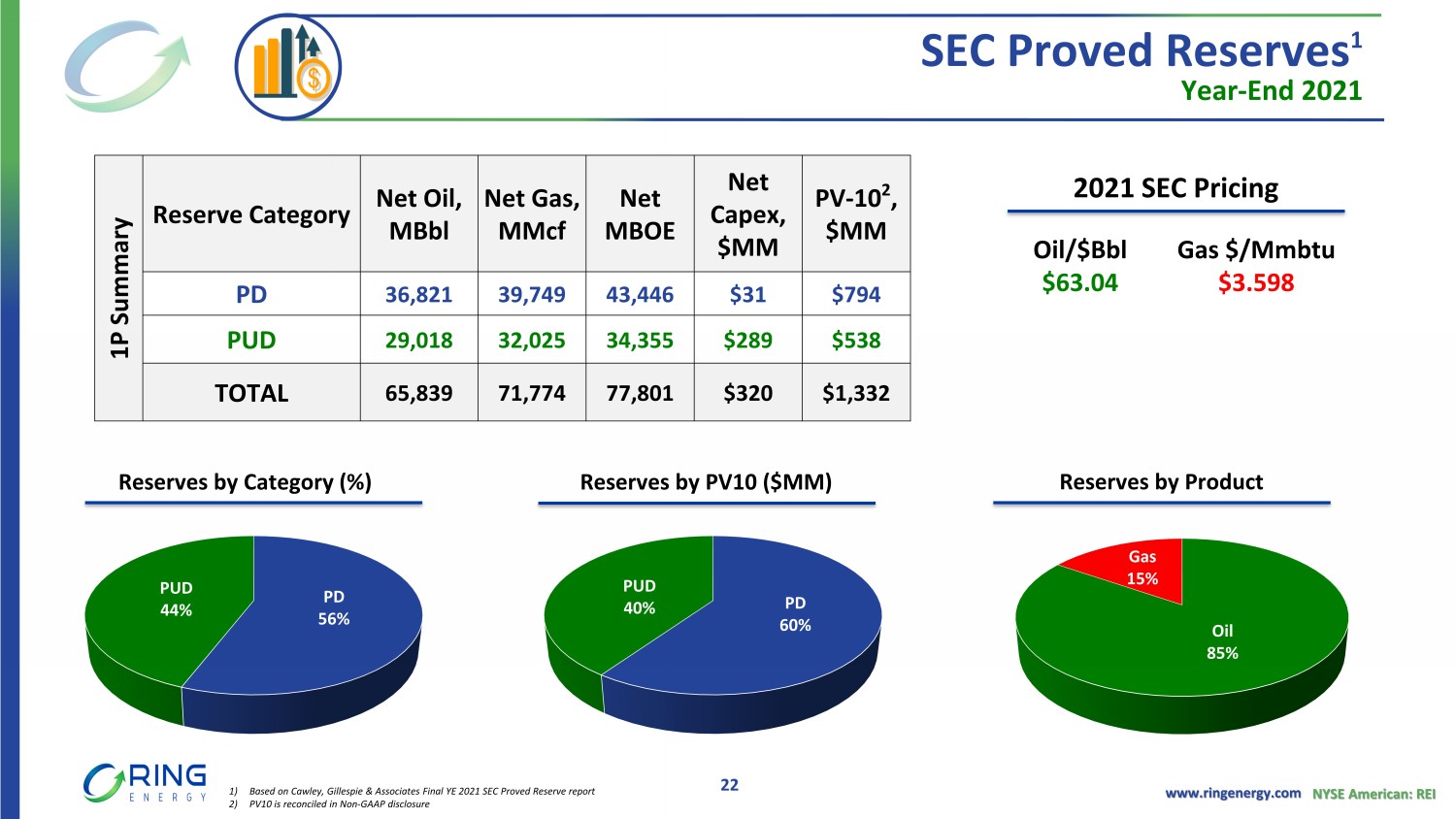

www.ringenergy.com NYSE American: REI PD 60% PUD 40% 1P Summary Reserve Category Net Oil, MBbl Net Gas, MMcf Net MBOE Net Capex, $MM PV - 10 2 , $MM PD 36,821 39,749 43,446 $31 $794 PUD 29,018 32,025 34,355 $289 $538 TOTAL 65,839 71,774 77,801 $320 $1,332 SEC Proved Reserves 1 Year - End 2021 2021 SEC Pricing Reserves by Category ( % ) Reserves by PV 10 ( $ MM) Reserves by Product Oil/$ Bbl $63.04 Gas $/ Mmbtu $3.598 Oil 85% Gas 15% PD 56% PUD 44% 1) Based on Cawley, Gillespie & Associates Final YE 2021 SEC Proved Reserve report 2) PV10 is reconciled in Non - GAAP disclosure 22

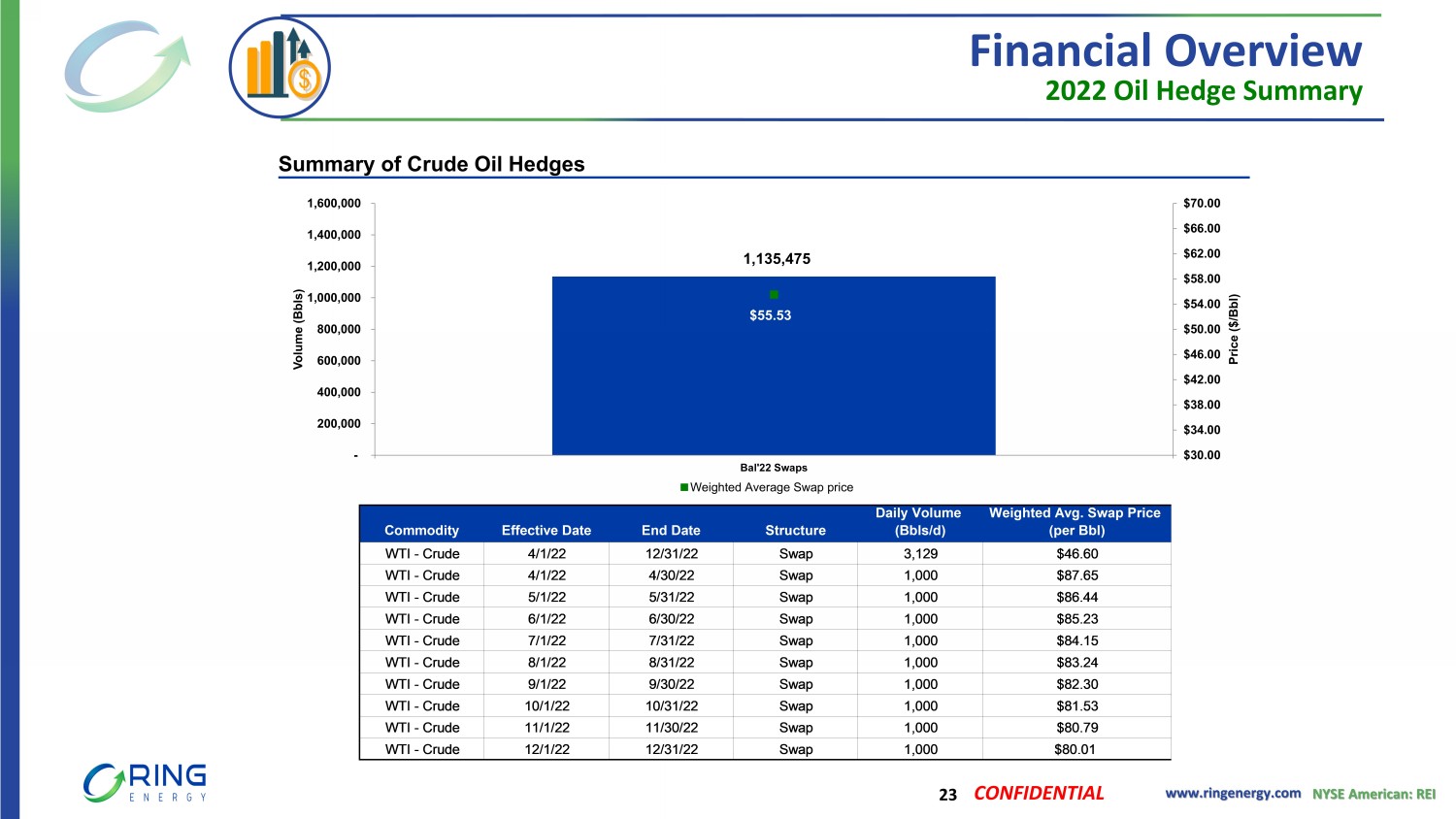

www.ringenergy.com NYSE American: REI Financial Overview 2022 Oil Hedge Summary Summary of Crude Oil Hedges CONFIDENTIAL 1,135,475 $55.53 $30.00 $34.00 $38.00 $42.00 $46.00 $50.00 $54.00 $58.00 $62.00 $66.00 $70.00 - 200,000 400,000 600,000 800,000 1,000,000 1,200,000 1,400,000 1,600,000 Bal'22 Swaps Price ($/Bbl) Volume (Bbls) Weighted Average Swap price 23 Commodity Effective Date End Date Structure Daily Volume (Bbls/d) Weighted Avg. Swap Price (per Bbl) WTI - Crude 4/1/22 12/31/22 Swap 3,129 $46.60 WTI - Crude 4/1/22 4/30/22 Swap 1,000 $87.65 WTI - Crude 5/1/22 5/31/22 Swap 1,000 $86.44 WTI - Crude 6/1/22 6/30/22 Swap 1,000 $85.23 WTI - Crude 7/1/22 7/31/22 Swap 1,000 $84.15 WTI - Crude 8/1/22 8/31/22 Swap 1,000 $83.24 WTI - Crude 9/1/22 9/30/22 Swap 1,000 $82.30 WTI - Crude 10/1/22 10/31/22 Swap 1,000 $81.53 WTI - Crude 11/1/22 11/30/22 Swap 1,000 $80.79 WTI - Crude 12/1/22 12/31/22 Swap 1,000 $80.01

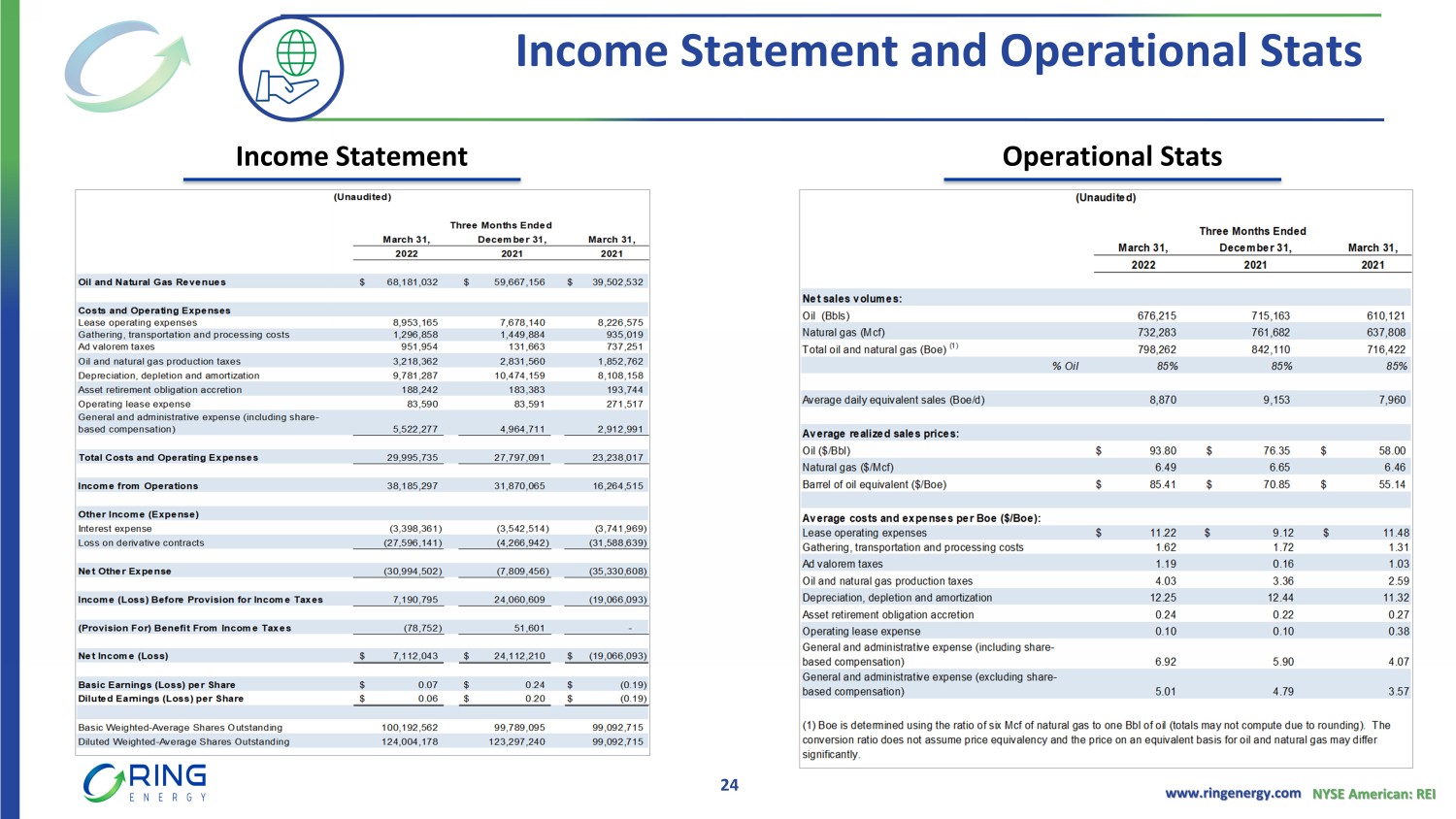

www.ringenergy.com NYSE American: REI Income Statement and Operational Stats Income Statement Operational Stats 24

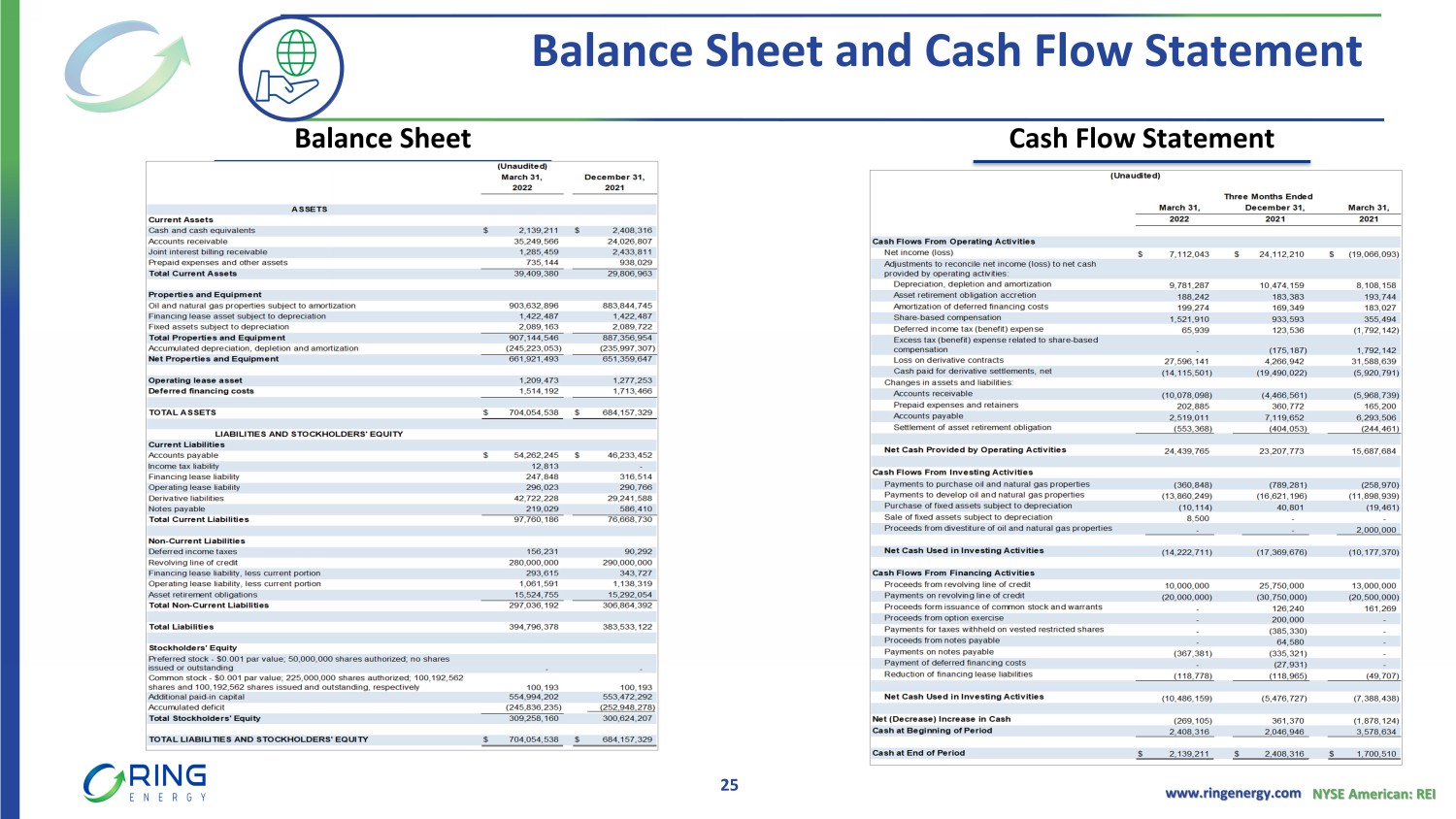

www.ringenergy.com NYSE American: REI Balance Sheet and Cash Flow Statement Balance Sheet Cash Flow Statement 25

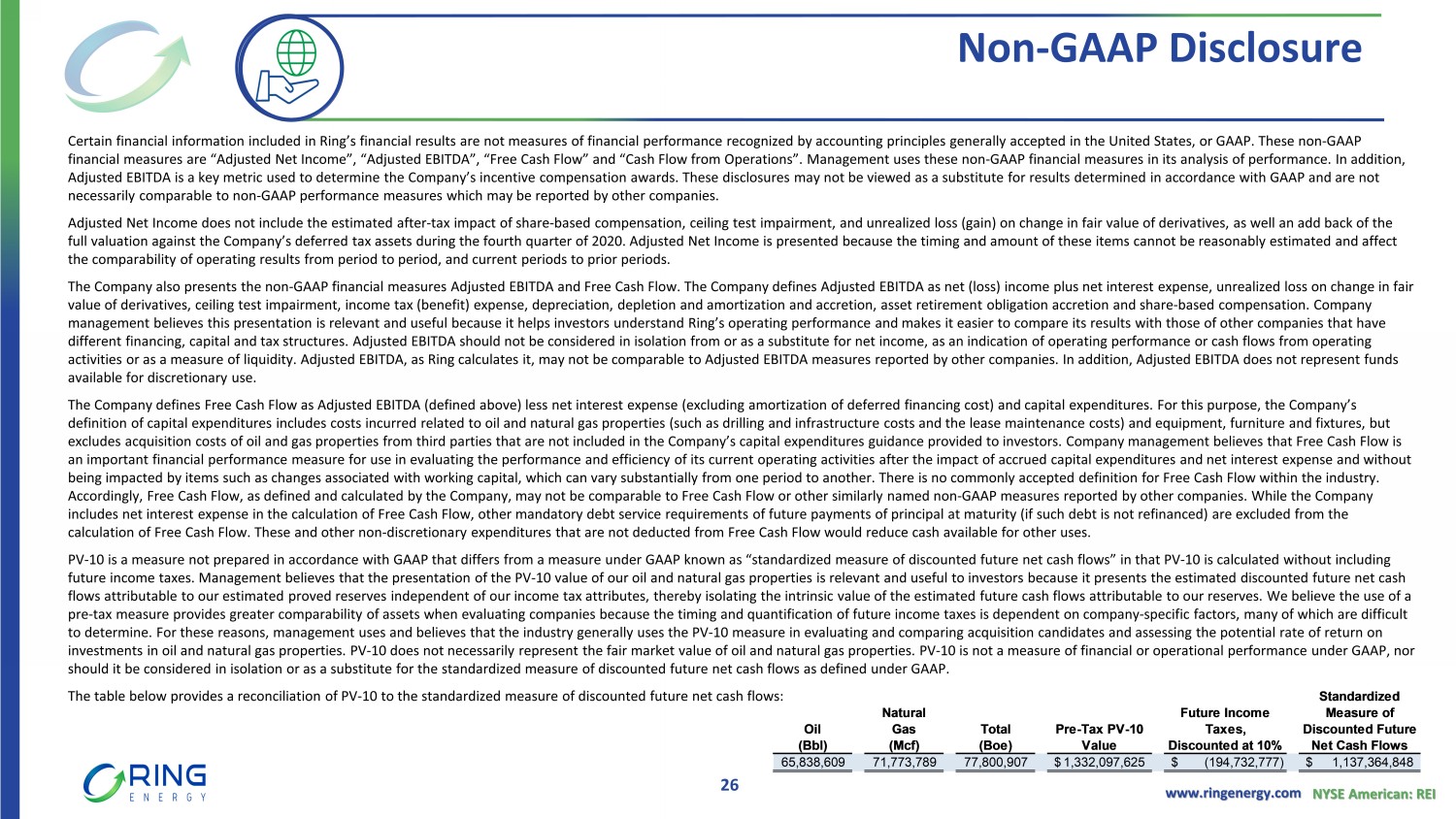

www.ringenergy.com NYSE American: REI Non - GAAP Disclosure Certain financial information included in Ring’s financial results are not measures of financial performance recognized by ac cou nting principles generally accepted in the United States, or GAAP. These non - GAAP financial measures are “Adjusted Net Income”, “Adjusted EBITDA”, “Free Cash Flow” and “Cash Flow from Operations”. Management us es these non - GAAP financial measures in its analysis of performance. In addition, Adjusted EBITDA is a key metric used to determine the Company’s incentive compensation awards. These disclosures may not be v iew ed as a substitute for results determined in accordance with GAAP and are not necessarily comparable to non - GAAP performance measures which may be reported by other companies. Adjusted Net Income does not include the estimated after - tax impact of share - based compensation, ceiling test impairment, and un realized loss (gain) on change in fair value of derivatives, as well an add back of the full valuation against the Company’s deferred tax assets during the fourth quarter of 2020. Adjusted Net Income is presented bec ause the timing and amount of these items cannot be reasonably estimated and affect the comparability of operating results from period to period, and current periods to prior periods. The Company also presents the non - GAAP financial measures Adjusted EBITDA and Free Cash Flow. The Company defines Adjusted EBITD A as net (loss) income plus net interest expense, unrealized loss on change in fair value of derivatives, ceiling test impairment, income tax (benefit) expense, depreciation, depletion and amortization and acc ret ion, asset retirement obligation accretion and share - based compensation. Company management believes this presentation is relevant and useful because it helps investors understand Ring’s operating performan ce and makes it easier to compare its results with those of other companies that have different financing, capital and tax structures. Adjusted EBITDA should not be considered in isolation from or as a substitut e f or net income, as an indication of operating performance or cash flows from operating activities or as a measure of liquidity. Adjusted EBITDA, as Ring calculates it, may not be comparable to Adjusted EBITDA mea sur es reported by other companies. In addition, Adjusted EBITDA does not represent funds available for discretionary use. The Company defines Free Cash Flow as Adjusted EBITDA (defined above) less net interest expense (excluding amortization of de fer red financing cost) and capital expenditures. For this purpose, the Company’s definition of capital expenditures includes costs incurred related to oil and natural gas properties (such as drilling and in fra structure costs and the lease maintenance costs) and equipment, furniture and fixtures, but excludes acquisition costs of oil and gas properties from third parties that are not included in the Company’s capital expend itu res guidance provided to investors. Company management believes that Free Cash Flow is an important financial performance measure for use in evaluating the performance and efficiency of its current operating acti vit ies after the impact of accrued capital expenditures and net interest expense and without being impacted by items such as changes associated with working capital, which can vary substantially from one period to anot her . There is no commonly accepted definition for Free Cash Flow within the industry. Accordingly, Free Cash Flow, as defined and calculated by the Company, may not be comparable to Free Cash Flow or other simil arl y named non - GAAP measures reported by other companies. While the Company includes net interest expense in the calculation of Free Cash Flow, other mandatory debt service requirements of future payme nts of principal at maturity (if such debt is not refinanced) are excluded from the calculation of Free Cash Flow. These and other non - discretionary expenditures that are not deducted from Free Cash Flow would re duce cash available for other uses. PV - 10 is a measure not prepared in accordance with GAAP that differs from a measure under GAAP known as “standardized measure of discounted future net cash flows” in that PV - 10 is calculated without including future income taxes. Management believes that the presentation of the PV - 10 value of our oil and natural gas properties is relev ant and useful to investors because it presents the estimated discounted future net cash flows attributable to our estimated proved reserves independent of our income tax attributes, thereby isolating the intrinsic va lue of the estimated future cash flows attributable to our reserves. We believe the use of a pre - tax measure provides greater comparability of assets when evaluating companies because the timing and quantification of futu re income taxes is dependent on company - specific factors, many of which are difficult to determine. For these reasons, management uses and believes that the industry generally uses the PV - 10 measure in evaluating a nd comparing acquisition candidates and assessing the potential rate of return on investments in oil and natural gas properties. PV - 10 does not necessarily represent the fair market value of oil and natural gas properties. PV - 10 is not a measure of financial or operational performance under GAAP, nor should it be considered in isolation or as a substitute for the standardized measure of discounted future net cash flows as d efi ned under GAAP. The table below provides a reconciliation of PV - 10 to the standardized measure of discounted future net cash flows: 26

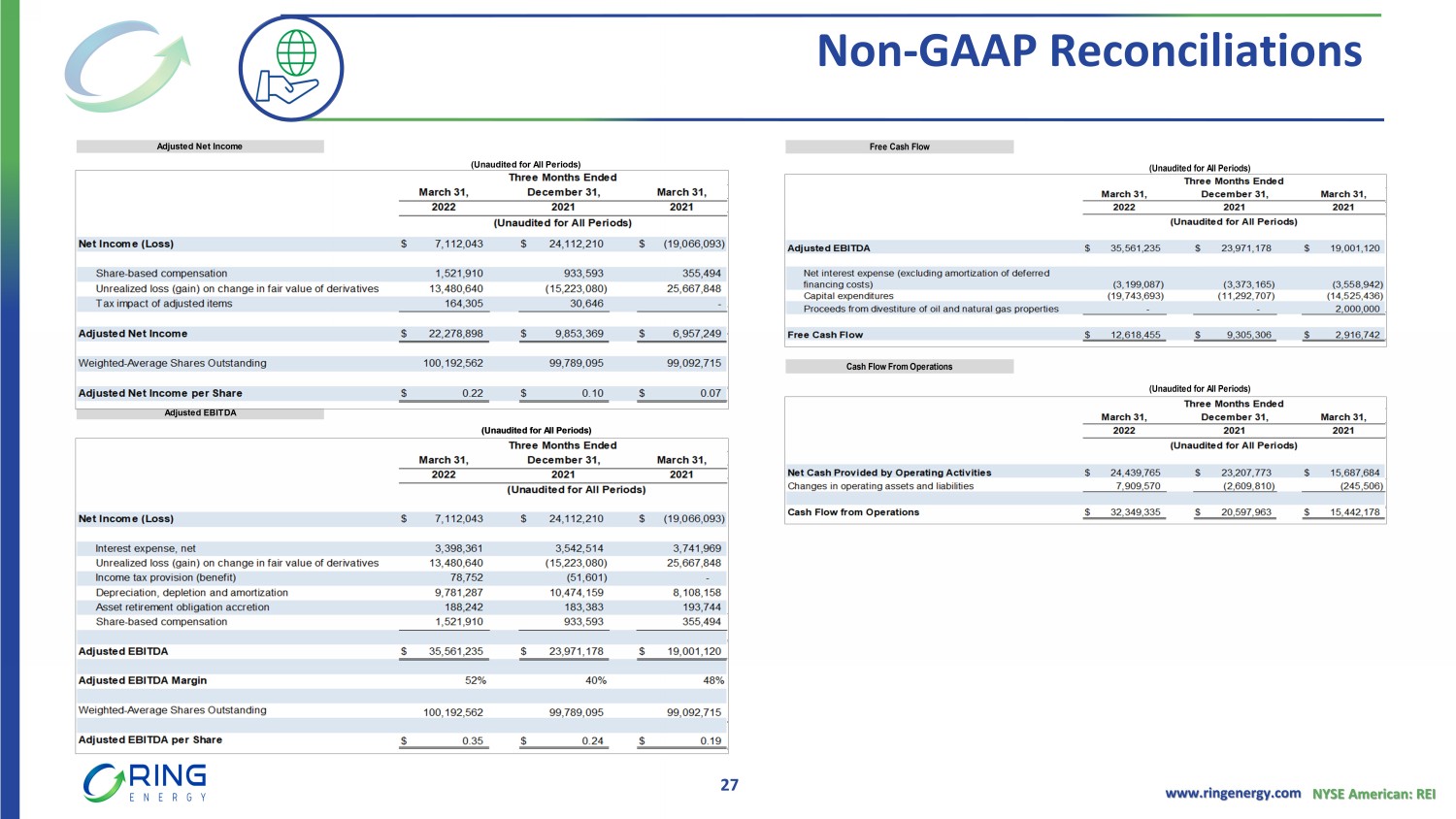

www.ringenergy.com NYSE American: REI Non - GAAP Reconciliations 27 Net Income (Loss) $ 24,112,210 $ 14,163,934 $ (160,254,277) $ 3,322,892 $ (253,411,828) Share-based compensation 933,593 777,461 2,807,006 2,418,323 5,364,162 Ceiling test impairment - - 129,564,000 - 277,501,943 Unrealized loss (gain) on change in fair value of derivatives (15,223,080) (8,200,688) 15,243,222 25,084,987 1,156,523 Tax impact of adjusted items 30,646 25,612 19,126,056 (225,432) (9,915,293) Adjusted Net Income $ 9,853,369 $ 6,766,319 $ 6,486,007 $ 30,600,770 $ 20,695,507 Weighted-Average Shares Outstanding 99,789,095 99,358,504 87,503,079 99,387,028 72,891,310 Adjusted Net Income per Share $ 0.10 $ 0.07 $ 0.07 $ 0.31 $ 0.28 Net Income (Loss) $ 24,112,210 $ 14,163,934 $ (160,254,277) $ 3,322,892 $ (253,411,828) Interest expense, net 3,542,514 3,551,462 4,658,825 14,490,473 17,617,606 Unrealized loss (gain) on change in fair value of derivatives (15,223,080) (8,200,688) 15,243,222 25,084,987 1,156,523 Ceiling test impairment - - 129,564,000 - 277,501,943 Income tax (benefit) expense (51,601) (48,701) 21,152,105 90,342 (6,001,176) Depreciation, depletion and amortization 10,474,159 9,310,524 11,162,567 37,167,967 43,010,660 Asset retirement obligation accretion 183,383 182,905 212,503 744,045 906,616 Share-based compensation 933,593 777,461 2,807,006 2,418,323 5,364,162 Adjusted EBITDA $ 23,971,178 $ 19,736,897 $ 24,545,951 $ 83,319,029 $ 86,144,506 Adjusted EBITDA Margin 40% 40% 78% 42% 76% Weighted-Average Shares Outstanding 99,789,095 99,358,504 87,503,079 99,387,028 72,891,310 Adjusted EBITDA per Boe $ 28.47 $ 26.02 $ 28.67 $ 26.80 $ 26.78 Adjusted EBITDA per Share $ 0.24 $ 0.20 $ 0.28 $ 0.84 $ 1.18 December 31, December 31, Twelve Months Ended Adjusted Net Income Adjusted EBITDA 2021 December 31, December 31, December 31, 2021 2020 Twelve Months Ended (Unaudited for All Periods) Three Months Ended December 31, 20202021 2021 2020 September 30, Three Months Ended September 30, December 31,December 31, 2021 (Unaudited for All Periods) 2021 2020

www.ringenergy.com NYSE American: REI Corporate Strategy Value Focused for Sustainable Success Attract and Retain Highly Qualified People Pursue Operational Excellence with a Sense of Urgency Invest in High - Margin, High RoR Projects Focus on FCF and Strengthen Balance Sheet Pursue Strategic A&D to Lower Breakeven Costs 28

www.ringenergy.com NYSE American: REI Add Photo Add Photo Add Photo Add Photo Add Photo Paul D. McKinney Chairman & Chief Executive Officer 35+ years of domestic & international oil & gas industry experience Executive & board roles include CEO, President, COO, Region VP and public & private board directorships Travis Thomas EVP & Chief Financial Officer 17+ years of oil & gas industry experience & accounting experience High level financial experience including CAO, VP Finance, Controller, Treasurer Alexander Dyes EVP of Engineering & Corporate Strategy 15+ years of oil & gas industry experience Multi - disciplined experience including VP A&D, VP Engineering, Director Strategy, multiple engineering & operational roles Marinos Baghdati EVP of Operations 19+ years of oil & gas industry experience Operational experience in drilling, completions and production including VP Operations, Operations manager, multiple engineering roles Stephen D. Brooks EVP of Land, Legal, HR & Marketing 40+ years of oil & gas industry experience Extensive career as landman including VP Land & Legal, VP HR VP Land and Land Manager Hollie Lamb VP of Compliance & GM of Midland Office 20+ years of oil & gas industry experience Previously Partner of HeLMS Oil & Gas, VP Engineering, Reservoir & Geologic Engineer Experienced Management Team Shared Vision with a Track Record of Success 29

www.ringenergy.com NYSE American: REI 30 Add Photo Paul D. McKinney Chairman & Chief Executive Officer 35+ years of domestic & international oil & gas industry experience Executive & board roles include CEO, President, COO, Region VP and public & private board directorships Anthony D. Petrelli Lead Independent Director 43+ years of banking, capital markets, governance & financial experience Executive and Board positions include CEO, President, multiple board chairs & directorships John A. Crum Independent Director 45+ years of domestic & international oil & gas industry experience Extensive executive roles including CEO, President & COO, and multiple public & private board chairs & directorships Richard E. Harris Independent Director 40+ years of experience across multiple industries Executive positions in oil & gas, industrial equipment, and technology including CIO, Treasurer, Finance and Business Development Thomas L. Mitchell Independent Director 35+ years of domestic & international oil & gas industry experience Executive & board roles include CFO, VP Accounting, Controller and public & private board directorships Regina Roesener Independent Director 35+ years of banking, capital markets, governance & financial experience Executive and Board positions including COO, director and Board Director positions Refreshed Board of Directors Accomplished and Diversified Experience Clayton E. Woodrum Independent Director 50+ years of accounting, tax & finance experience Wide range of financial acumen including positions as CFO, Partner in Charge and Board Director positions

ANALYST COVERAGE Alliance Global Partners (A.G.P.) Jeff Campbell (203) 577 - 5427 jcampbell@allianceg.com Tuohy Brothers Investment Noel Parks (215) 913 - 7320 nparks@tuohybrothers.com ROTH Capital Partners John M. White (949) 720 - 7115 jwhite@roth.com Truist Financial Neal Dingmann (713) 247 - 9000 neal.dingmann@truist.com COMPANY CONTACT Al Petrie (281) 975 - 2146 apetrie@ringenergy.com Chris Delange (281) 975 - 2146 cdelange @ringenergy.com